The Paradox in India’s Fintech Expansion

Syna Karnani | Pablo Ventura Admirall

At the heart of India’s recent economic boom lies its digital revolution. This digital revolution is centred around the Unified Payments Interface (UPI), an instant real-time payment system developed by the National Payments Corporation of India (NPCI); a state-created non-profit owned by 56 banks ranging from public to private sector to manage retail payment infrastructure. Soon after its 2016 launch, UPI became the backbone of India’s fintech ecosystem, recording over 20 billion transactions worth 24.85 trillion dollars—the highest ever in the country’s digital payments history—in August 2025 alone. This rapid adoption has been driven by a combination of a tech-savvy population and the government’s Digital India scheme. As a result, India is set to have over 900 million internet users by the end of 2025. This shift has allowed millions of small business owners and freelancers to enter the formal financial market for the first time. By enabling instant, low-cost digital payments, UPI has stimulated domestic demand, encouraged entrepreneurship, and inspired innovation across sectors. However, while UPI has broken old barriers to financial access, it has also created new forms of barriers through algorithmic governance and regulatory imbalance.

In the early 2000s India’s rural households had limited access to financial services. Over half of all rural households (59 percent) did not have an account with a formal financial institution. India’s first credit rating agency was established in 2000 so most people lacked formal credit histories. Further, more than 90% of retail transactions were conducted in cash. To address this the government launched the Digital India Scheme in 2015. It increased internet use and digital literacy, paving the way for the Unified Payments Interface. UPI allows users to transfer money instantly between bank accounts by using a smartphone instead of a physical card. However, analysis based on NPCI documentation reveals that every UPI transaction generates a stream of data. This information ranges from who the user is, to the type of device they use. Once collected, this data is processed through algorithms that automate tasks such as fraud detection, credit scoring, and product recommendations. In theory this makes financial services faster and more efficient. In practice, however, inclusion no longer depends on whether someone wants to be part of the digital economy, it depends on whether their data profiles meet the thresholds set by these algorithms. This favours urban users with frequent transactions, while rural or low-income users who are often reliant on cash and face poor connectivity issues appear “risky”. Consider, for example, a shopkeeper in a rural village who still relies heavily on cash because internet connectivity is patchy and customers prefer cash for small purchases. Even if this merchant uses UPI occasionally, their digital footprint appears sparse compared to an urban professional who pays for groceries, transport, and entertainment digitally every day. The algorithm may flag the shopkeeper as “risky” simply because their transaction data is limited, not because they are actually unreliable. As a result, without scrutiny, these algorithmic decisions, such as who gets credit and who is flagged as risky, become invisible forms of inequality. The paradox of UPI, then, lies in the fact that what was once celebrated as a means of inclusivity now restricts it by the biases embedded in code.

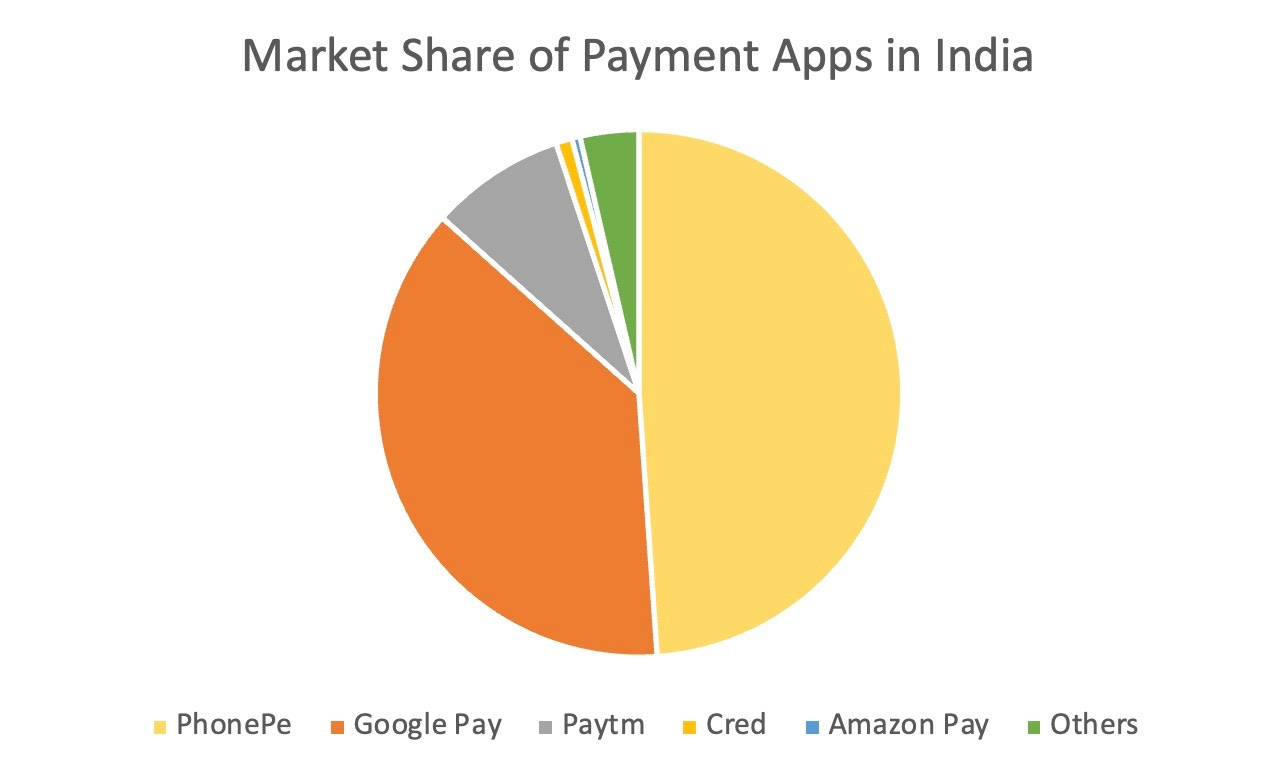

The biggest structural challenge associated with UPI lies in the policy’s inability to keep pace with innovation. The pace of UPI’s expansion has been so rapid that its scale now exceeds the capacity of existing competition and government regulations to manage it effectively. As of 2024, two dominant players, PhonePe and Google Pay, together control more than 80% of transactions.

This dominance did not emerge by accident. Both companies invested heavily in user acquisition through cashback schemes. Further, their early partnerships with banks and merchants created strong network effects: the more people used these platforms, the more valuable they became, which in turn attracted even more users. For many consumers, especially first‑time digital payment users, these apps became the default gateways into UPI, crowding out smaller competitors even as they matched features and spending. This level of market concentration has drawn concern from the Reserve Bank of India, prompting them to propose a 30% cap on any single platform’s market share, but implementation of this regulation has been postponed till 2026. This highlights a common struggle in emerging markets: policymakers are hesitant to restrict platforms that have stimulated financial inclusion; however, in doing so, they bear the risk of allowing near monopolies to form. The issue extends further than market share, becoming one of influence. These platforms have become essential intermediaries between consumers, merchants, and banks, giving them disproportionate power to shape consumer experiences. For example, they can prioritize certain transactions, promote preferred merchants, or design incentive structures that steer users toward specific services. A fintech startup offering innovative payment solutions may struggle to gain visibility because it must integrate through the very platforms it hopes to disrupt. Similarly, micro‑merchants often depend on promotional incentives, such as discounts or featured listings, to attract customers. If these incentives are withdrawn or restructured, their sales can collapse overnight. In this way, the platforms become “gatekeepers,” determining not only how transactions occur but also who thrives in the digital marketplace. Without a governing structure to address competition, India’s digital finance sector risks reproducing offline inequalities in a digital form. Therefore, effective oversight must change from reactive intervention to anticipatory regulations, one that encourages innovation while preventing any single actor from controlling the infrastructure of inclusion.

Algorithmic governance now determines which users and merchants gain visibility, while regulatory delays allow platforms to consolidate power. Together, these issues create the paradox at the heart of India’s digital economy, the same infrastructure that expands access can also concentrate control. The challenge, then, is not to slow innovation but to ensure its benefits are shared more evenly. The Reserve Bank of India’s Digital Payments Index now incorporates data‑security standards and grievance‑redress mechanisms, signaling a move toward greater accountability. Similarly, India Stack promotes interoperability, preventing the digital economy from being locked inside a few corporate platforms. Yet these steps remain partial. Stronger reforms are needed. For example, independent audits of algorithms to check for bias, enforceable limits on platform dominance to preserve competition, and safeguards that prevent the costs of digitization from overwhelming small businesses. These reforms would directly tackle exclusion and concentration, reinforcing the inclusivity that made UPI successful in the first place.

The rise of India’s fintech sector is one of the most compelling economic narratives of the past decade. This “made in India” model combines innovation, policy, and mass adoption. Yet digital inclusion that offers access without meaningful control risks falling short of true empowerment. Participation through highly centralized systems can create new forms of dependence, even as it expands opportunities. The focus must shift from counting transactions to examining who controls them and under what terms. By ensuring transparency and competition in its fintech economy, India can safeguard stability while offering a blueprint for other emerging markets. The promise of digital inclusion, then, should be measured not only by the volume of transactions but by the quality of participation: how equitable, secure, and genuinely empowering it proves to be.

Syna is a freshman at Barnard College of Columbia University, class of 2029, where she is studying economics and mathematics. She grew up in Mumbai, India’s financial capital, and saw firsthand how UPI affected the way people paid, saved, and participated in the economy. Syna has become fascinated by the way economics can shape everyday life and how public policy can expand or limit opportunity. Studying economics and mathematics gives her the knowledge to explore those connections, but what excites her most is asking bigger questions, about inclusion, fairness, and the systems we build to govern ourselves.

| A guest post by

|