Indonesia’s Downstreaming Gambit: Investment Gains and Industrial Constraints

Syna Karnani | Pablo Ventura Admirall

In 2020, Indonesia implemented a significant act of resource nationalism by enforcing a ban on exports of unprocessed nickel ore, thereby using state power to keep raw materials at home and force foreign investors to build value-adding capacity inside the country. Indonesia used its dominant resource position to coerce investment in domestic manufacturing and refining of battery materials. The headline results were striking: earnings from nickel exports increased from low single-digit billions in the early 2010s to 30 billion dollars by 2022. As the primary input for high-energy-density cathodes used in electric vehicle (EV) batteries, nickel is among the most strategically important minerals of the 21st century. Following the ban, Indonesia’s share of global nickel output rose sharply; it now controls more than 60% of global nickel mining supply. From Jakarta’s perspective, the policy established that a single, well-targeted act of resource nationalism could move Indonesia from the commodity periphery closer to the center of the electric-vehicle supply chain.

This article argues that while the nickel export ban succeeded in attracting investment and building processing capacity into Indonesia, it has not yet produced the industrial foundations that the policy was meant to create. To explore this thesis, the article first examines how the post-ban nickel boom created a new dependence on Chinese firms in Indonesia’s downstreaming, which refers to the processing of nickel locally; it then assesses how changing battery chemistry, particularly the growth of LFP, threatens the demand assumptions the ban was based on; and finally, it evaluates whether and how Indonesia can adapt its policy into a more resilient industrial strategy.

The China Problem

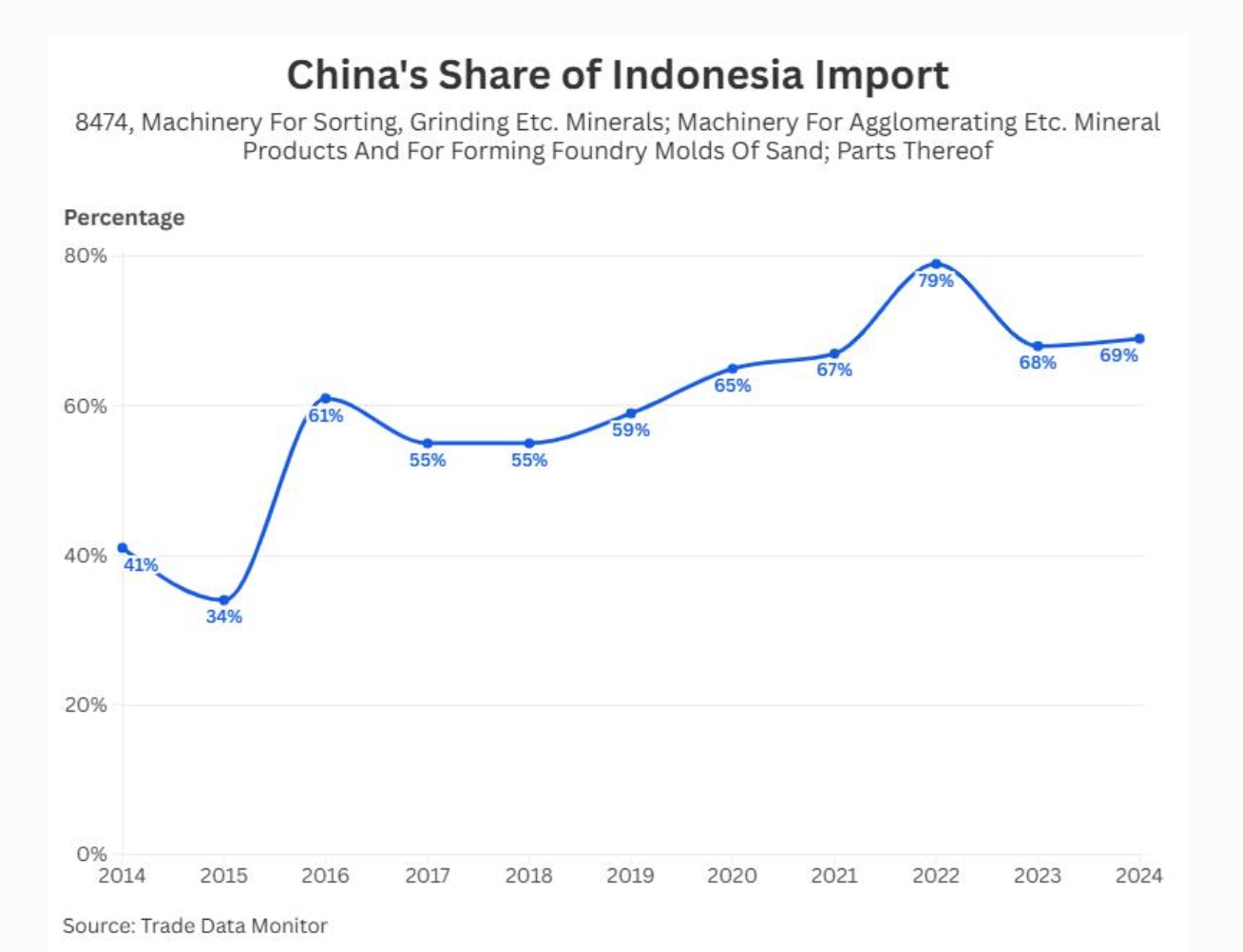

The immediate winners of Indonesia’s export ban were often Chinese firms, whose capital and technology allowed them to dominate the newly created downstream segments and thereby limit Indonesia’s control over the value chain. Chinese firms financed and now control most of the refining capacity built after the export ban. They capture a large share of the value created by Indonesia’s downstreaming process and shape how that value is distributed. A Pacific Forum brief estimates that following the 2019 export ban, Chinese firms quickly and vastly invested in nickel and critical mineral processing facilities equal to $30 billion. The same analysis reports that the number of nickel smelters rose from 2 in 2016 to more than 60 by 2024, fueled by foreign direct investment in processing facilities. By 2023, Chinese enterprises controlled around 75% of Indonesia’s roughly 8-million-tonne nickel refining capacity. Of this 75%, two firms–Tsingshan Holding Group and Jiangsu Delong Nickel Industry- account for more than 70%. These companies provided the capital for new smelters and industrial parks, supplied most of the processing equipment and technology, and locked in offtake agreements as primary buyers of the refined nickel. In 2024, Indonesia consistently imported 70% of heavy machinery used for mineral ores from China, valuing over $750 million. This has more than doubled from just over $300 million in 2014.

Figure 1: Graph depicting China’s share of Indonesian Import

On paper, this new infrastructure exists on Indonesian soil; in practice, the key decisions about technology choices, prices, and reinvestment are made in Chinese corporate headquarters.

This is significant because the foundation of the ban was rooted in the fact that forcing domestic production would give Indonesia a larger share of the value embedded in its resources. What resulted, instead, is a vertical integration of Chinese industry onto Indonesian territory. As a result, Indonesia has climbed the nickel value chain, without gaining meaningful control over it.

In the short run, this arrangement suited both parties. China secured long-term battery material supply as its electric-vehicle industry expanded, while Indonesia posted the investment and growth numbers it needed as visible proof of downstreaming success. Some Indonesian firms have benefited directly from the Chinese investment, particularly state-owned enterprises like MIND ID, but official statements and project structures indicate that they still rely heavily on foreign investors for finance, technology, and market access. This structural asymmetry produced resembles the upstream-downstream relationship that the ban was designed to escape, replicated now inside Indonesia’s own border rather than across borders. Genuine industrial development requires more than just processing capability. It requires the accumulation of technological knowledge, managerial expertise, and domestic capital that can outlast any single commodity cycle. On those measures, the ban’s returns have been limited, with relatively little high-end processing knowledge or ownership migrating into Indonesian hands. Thus, while downstream capacity has expanded within Indonesia, much of the control over that capacity remains external.

The LFP Question

Even if Indonesia can resolve its dependency on Chinese capital and operators, a second vulnerability, evolving battery technology, threatens the demand foundations of its nickel strategy and further constrains its ability to turn its leverage into lasting industrial power. The export ban was established based on a particular vision of where the electric vehicle industry was headed: a world in which nickel-rich cathode chemistries dominated battery production, making Indonesia an indispensable supplier as EV penetration scaled globally. That assumption is no longer secure. Lithium iron phosphate batteries (LFP), which use no nickel whatsoever, have rapidly and unexpectedly gained market share. LFP batteries reached an estimated 40% of global EV battery capacity sold in 2023, closing much of the energy-density gap with nickel-based alternatives while retaining a cost advantage of roughly 20-30% per kilowatt-hour.

A 2026 market review finds that LFP is becoming the default chemistry for entry-level and budget EVs because of lower cost and improving performance. The implications for Indonesia are direct. If standard and budget-range EVs (the fastest-growing segment of the global market) consolidate around LFP while only high-performance, long-range vehicles retain nickel-based cathodes, the addressable market for battery-grade Indonesian nickel may be substantially smaller than the projections that animated the investment wave of 2020 to 2023. Indonesia could emerge from this decade with excess refining capacity, billions of dollars of smelters and HPAL facilities, built for a demand trajectory that battery technology has already begun to flatten. The export ban was designed to ride the EV supercycle; it did not build in a mechanism for responding if the supercycle shifted to a chemistry that largely bypasses nickel.

Critically, Indonesia has limited leverage over this risk. The LFP shift is driven by decisions made in Chinese and European battery laboratories and by the price-sensitive consumers choosing mass-market EVs, not by industrial policy in Jakarta. The country can control whether raw ore leaves its borders; it cannot control whether the batteries its ore is destined for remain the batteries the market wants. Analysts at the ISEAS-Yusof Ishak Institute have suggested that Indonesia move away from an all-or-nothing export ban toward a more flexible domestic market obligation framework, in which the state would guarantee a baseline of ore for domestic processors while retaining the ability to adjust export volumes in response to market signals. Such a system would not solve the LFP problem, but it would give policymakers more tools to respond to demand shifts than the current binary approach. As a result of this demand shift, the long-term viability of Indonesia’s nickel strategy depends on demand conditions that are increasingly shaped outside its control.

A Durable Model?

Taken together, the China dependency and the LFP risk reveal the core tension in Indonesia’s nickel strategy: the policy has been spectacularly effective in capturing a particular moment in global demand, but it has not yet built the foundations for durable industrialization grounded in domestic control. The export ban succeeded in its immediate objectives, but it did so by optimizing for a specific moment: peak demand for nickel-based battery chemistries, attracting investors who could deploy capital quickly, build smelters at scale, and plug Indonesian ore into existing global supply chains. It did far less to ensure that those investments would generate deep linkages into the domestic economy in the form of competitive Indonesian firms, locally embedded technological capabilities, or institutions capable of steering the sector as conditions change.

The question facing the Prabowo government is therefore not whether the nickel export ban “worked” in a narrow sense. It did: output expanded, value added increased, and Indonesia became central to the global nickel market. The more important question is whether the current model can be transformed from a one-off success into a development strategy that remains viable when the external environment becomes less forgiving. That transformation would require at least three shifts: diversifying the investor base beyond Chinese capital, introducing more flexible instruments for managing ore supply as battery chemistry evolves, and investing heavily in the institutional capacity needed to convert foreign-led projects into domestic technological upgrading. None of these steps would abandon the core logic of downstreaming. Instead, they would test whether Indonesia can use a moment of leverage in one commodity to construct a broader platform for industrial policy. For other resource-rich emerging economies, the lesson is not simply that export bans produce industrialization, but that they can create a window in which industrialization becomes possible if governments are willing to tackle the harder tasks of building state capacity, negotiating more demanding terms with investors, and planning for market shifts that may undermine today’s windfalls. Indonesia has already cleared a high bar by forcing global industry to reorganize around its ore; whether the current policy can evolve to address these constraints will determine its long-term role in Indonesia’s industrial development.

Syna is a freshman at Barnard College of Columbia University, class of 2029. She is fascinated by the way economics can shape everyday life and how public policy can expand or limit opportunity. Majoring in Economics and Mathematics gives her the knowledge to explore those connections, but what excites her most is asking bigger questions, about inclusion, fairness, and the systems we build to govern ourselves.

q

| A guest post by

|