Frozen Assets on the Polar Silk Road: China’s Strategic Bet on Arctic LNG

Annabelle Lu | Pablo Ventura Admirall

Photo Credit: U.S. Naval Institute, Public Domain

China’s Polar Silk Road, a component of the global Belt and Road Initiative (BRI) focused on developing Arctic shipping routes and infrastructure, is often portrayed as an effort to shorten Asia-Europe transit times or advance scientific polar research. Yet rather than prioritizing transit efficiency alone, a more consequential objective can be seen in China’s securing of equity and long-term offtake positions, or contracts that guarantee a fixed share of future output, in Arctic liquefied natural gas (LNG) projects. This development has shifted China from a price-taker to a stakeholder with priority supply access. As global LNG flows become increasingly politicized and supply chains are exposed to geopolitical risk, China’s deepening involvement in Arctic energy infrastructure, particularly the Yamal LNG and Arctic LNG 2 Plant projects, serves a strategic purpose beyond commercial returns. By financing, building, and securing long-term access to Arctic LNG production, China is quietly reducing dependence on volatile gas markets while enhancing its energy security for the next decade. The Polar Silk Road, therefore, allows China to redefine volatility by deliberately shifting risk away from its own future supply and onto the global energy system.

China’s participation in some of the largest Arctic LNG projects, notably Yamal LNG and Arctic LNG 2, demonstrates this strategy by enabling partial upstream control over Arctic energy production while reducing reliance on global spot markets. At Yamal LNG, which produces at or above its annual capacity of approximately 16.5 mmt, the China National Petroleum Corporation (CNPC) holds a 20 percent stake, the Silk Road Fund owns an additional 9.9 percent, and an additional $12 billion in Chinese financing proved critical amidst Western sanctions imposing restrictions on Russia’s access to capital markets. This involvement has generated two key benefits for China in the past decade, seen in the shared financial profit from Yamal LNG global exports for Chinese firms and preferential access to physical LNG shipments.

However, this control remains partial and constrained. Since LNG from Yamal is sold globally, China does not command full allocation of its output, and access is mediated by all contractual parties rather than China’s sovereign control. Arctic LNG 2, another Russian project led by the second-largest Russian natural gas producer, Novatek, further highlights these limitations. Although designed to reach 19.8 mmt annually, its development has been slowed by U.S. sanctions targeting financing, technology, and shipping, delaying full capacity beyond the initial 6.6 mt liquefaction train that began operating in 2023–2024. These constraints underscore a key tension in China’s strategy: while direct investment in Arctic LNG reduces exposure to market volatility, China remains vulnerable to secondhand geopolitical risk and delayed project development from its partnership with Russia. Even without full output control, China’s equity positions and offtake agreements allow it to secure a predictable share of production, insulating part of its energy supply from LNG price volatility.

Often underemphasized in analyses of the Polar Silk Road, the scale of Arctic LNG projects underscores their strategic potential in reducing Chinese exposure to energy volatility while simultaneously revealing the constraints of partial control in production. At full capacity, Yamal LNG and Arctic LNG 2 could produce a combined output of 36.3 mmt annually, the sum of 16.5 from Yamal and 19.8 from Arctic LNG 2. Compared with China’s 67 mt of LNG imports in 2025, this theoretical capacity would equal approximately 54.2 percent of China’s current LNG imports. However, in practice, not all of this production would be directed to China, as the produced LNG is diversified amongst global consumers, especially in the current environment where sanctions disrupt shipping and financing. Even so, if China were able to secure a meaningful share, such as 10–20 mt annually in proportion to its equity stake, Arctic LNG stands to comprise a meaningful portion of China’s long-term gas supply.

The shift towards upstream energy control is driven by vulnerabilities in China’s existing energy import structure, particularly an overt dependence on LNG passing through maritime chokepoints and politically-sensitive supply chains. According to the U.S. Energy Information Administration (EIA), China became the world’s largest LNG importer in 2023, surpassing Japan, as total LNG imports reached approximately 71 million metric tons (mmt).

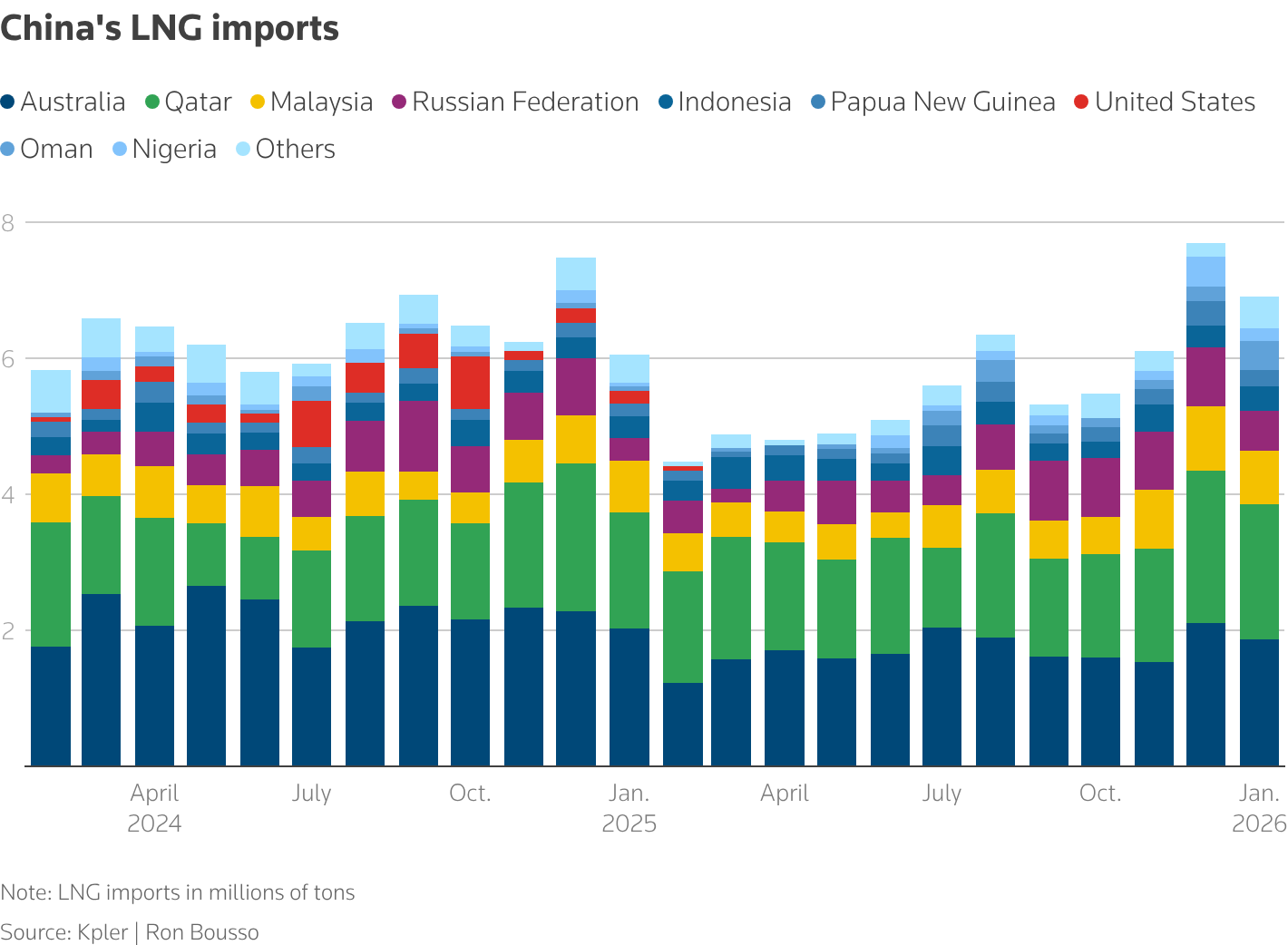

Figure 1. China’s LNG Imports. Source: Kpler; chart by Ron Bousso, Reuters.

As seen in Figure 1, these imports remain concentrated among a small group of suppliers led by Australia and Qatar, while Russia, Malaysia, and Indonesia also contribute significant and growing volumes. Chinese energy firms have additionally signed long-term supply agreements with American producers. According to Reuters, companies including PetroChina, CNOOC, and Unipec have signed nearly 20 LNG contracts with U.S. exporters that total around 25 million tons (mt) per year, with many agreements lasting 20–25 years. However, this demand uptick and prioritization of supply diversification is emerging as traditional supply routes face increasing geopolitical pressure. Many LNG shipments from the Middle East must pass through vulnerable maritime chokepoints, with around 20% of global flows passing through the Strait of Hormuz in Iran and around 23% across the Strait of Malacca, which lies between Sumatra and the Malay Peninsula. These routes are often exposed to geopolitical tensions, regional conflicts, and potential naval blockades, resulting in what Chinese strategists often describe as the “Malacca dilemma.” Furthermore, the presence of sanctions, namely those imposed by the U.S. and European Union (E.U.) on Russia following its invasion of Ukraine, has contributed to higher energy prices and supply constraints. In this environment, the mainstream narrative of seeking route diversification for energy corridors only partially shields Chinese demand from risk. China’s Arctic engagement therefore alternatively presents an opportunity to secure stable direct ownership in energy production while reducing major reliance on contested transit routes.

Domestic energy dynamics further reinforce the necessity of LNG diversification, as rising demand for natural gas continues to outpace domestic self-sufficiency. Over the past decade, Beijing has increasingly promoted natural gas as a transition fuel in order to reduce coal dependence and improve air quality in major cities, leading to consistent consumption growth that has increased reliance on imports. According to Duan Zhaofang, Head of Natural Gas Research at the China National Petroleum Corporation (CNPC), China’s natural gas consumption is expected to grow roughly five percent in 2026, driven primarily by industrial demand and recovery in exports after recent trade disruptions including tariffs, export controls, and regulatory restrictions. This follows an average annual growth rate of approximately eight percent since 2017, driven by both economic demand and policy incentives that have encouraged cleaner energy. Although domestic natural gas production is expanding, projected to reach “approximately 300 billion cubic meters by about 2030” as outlined in Beijing’s 15th Five-Year Plan (2026–2030), domestic output is unlikely to keep pace. Additionally, China has encouraged enterprise participation in Arctic ambitions through its 2018 Arctic Policy white paper, outlining the “exploitation of oil, gas, and mineral resources in the Arctic” while controversially coining itself a “near-Arctic state.” As such, China’s reliance on imported LNG appears to be an increasingly important economic fixture, increasing the value of securing stable long-term supply through overseas investments.

Russia has emerged as a central partner in this Arctic strategy, but also introduces clear geopolitical risk complications. In February 2026, Russia supplied China with more than 2 million barrels of Urals crude oil per day, cementing it as China’s largest oil exporter while remaining its second-largest LNG supplier (after Australia). This dual role highlights the growing concentration of China’s energy imports in a single partner. However, Russian LNG possesses rising strategic value: unlike oil, which is traded on volatile spot markets through real-time contract pricing, LNG supply has allowed China to secure predictably accessible long-term contracts through equity stakes and offtake agreements. This strategy has consequently been undermined by U.S. sanctions on Russian energy projects following the 2022 invasion of Ukraine, which have targeted financing, shipping insurance, and technology for projects such as Yamal LNG and Arctic LNG 2. At the same time, the European Union has announced plans to phase out Russian LNG imports by 2027: these restrictions have further slowed project timelines and reliability of supply transportation, particularly by targeting Russia’s so-called “shadow fleet” used to move sanctioned energy exports.

Sanctions have also raised participation costs for Chinese firms, shifting risk from volatility exposure to operations and bargaining. In June 2024, Chinese engineering firm Wison New Energies withdrew from Arctic LNG 2 construction under Western pressure, while subsequent reports suggested that Chinese ships continued delivery of large power-generation modules to the site under more opaque conditions to avoid sanctions reinforcement. These disruptions exemplify how geopolitical constraints can directly delay construction and complicate project execution. Conversely, sanctions have strengthened bilateral energy dependence, allowing China to become a primary buyer and partner amidst reduced Western purchasing of Russian LNG and oil. This relationship has been recently reinforced by major infrastructure projects such as the 4,188-km Eastern Siberia-Pacific Ocean (ESPO) oil pipeline and the 5,111-km Power of Siberia natural gas pipeline, which were both designed to channel Russian energy exports directly into Asian markets. However, pricing and supply disagreements over the proposed Power of Siberia II pipeline, which sought to transport gas from Arctic fields into China, have highlighted the fragility of this relationship. China’s continued involvement therefore reflects a tradeoff between securing long-term LNG access while accepting absorption of secondary sanction effects and reduced bargaining leverage.

China’s investment in Arctic shipping infrastructure further complements its strategy by extending control over energy transportation routes. The Northern Sea Route (NSR), a September 2025 joint Russian venture running along Russia’s Arctic coastline, offers a shorter alternative to the Suez Canal for transporting LNG between Asia and Europe that has been bolstered by melting ice in the area. In support of this route, China has invested in specialized icebreaker LNG carrier ships and polar research vessels to expand its ability to operate in Arctic conditions: “industry projections suggest that as many as 15–17 nuclear icebreakers may be required to support projected cargo volumes of 100–150 mt annually along the NSR,” driven largely by Arctic exports of LNG, crude oil, and metals. Domestic shipyards now produce a growing range of research and “polar-capable” diesel-electric-propelled vessels that are able to navigate all-season conditions, including modern icebreakers such as Xue Long 2. Although China’s polar fleet is still limited to five ships, Beijing’s continued investment in specialized “heavy” ship design and polar-region engineering within the past two years advances a long-term effort to strengthen capabilities for Arctic vessels capturing commercial benefit, especially through reducing foreign reliance in the shadow of Russia’s 57 icebreaker fleet. While the NSR presents a unique challenge due to harsh conditions and seasonal constraints, China’s commitment to develop independent logistical capabilities not only facilitates Arctic energy transport, but reduces reliance on Western-controlled maritime infrastructure.

Ultimately, China’s Polar Silk Road reflects a strategic shift from open-market dependence toward increased control through Arctic energy supply. By securing equity stakes in Arctic LNG projects, investing in transport infrastructure, and deepening ties with Russia, China is not eliminating risk but reshaping it, exchanging exposure to energy pricing volatility for more concentrated geopolitical and operational risks, including sanctions pressure, project delays, and dependence on a single partner. If current Arctic projects eventually reach full production capacity, or if further initiatives are slowly resurrected over the next decade, Arctic LNG could supply tens of millions of tons of natural gas annually to not only China, but global markets, bolstered by its geopolitically-diversified advantage. In this sense, the Polar Silk Road is not merely a shipping corridor extended from the BRI, but a long-term energy strategy to anchor China’s LNG security by concentrating risk exposure from its growing energy demand within an expanded Arctic presence.

Annabelle Lu (BC ’28) is a writer for the Columbia Emerging Markets Review studying Economics with a concentration in Political Economy. She is interested in the geopolitical, cultural, and technological dynamics that are currently shaping investment and innovation in emerging markets.